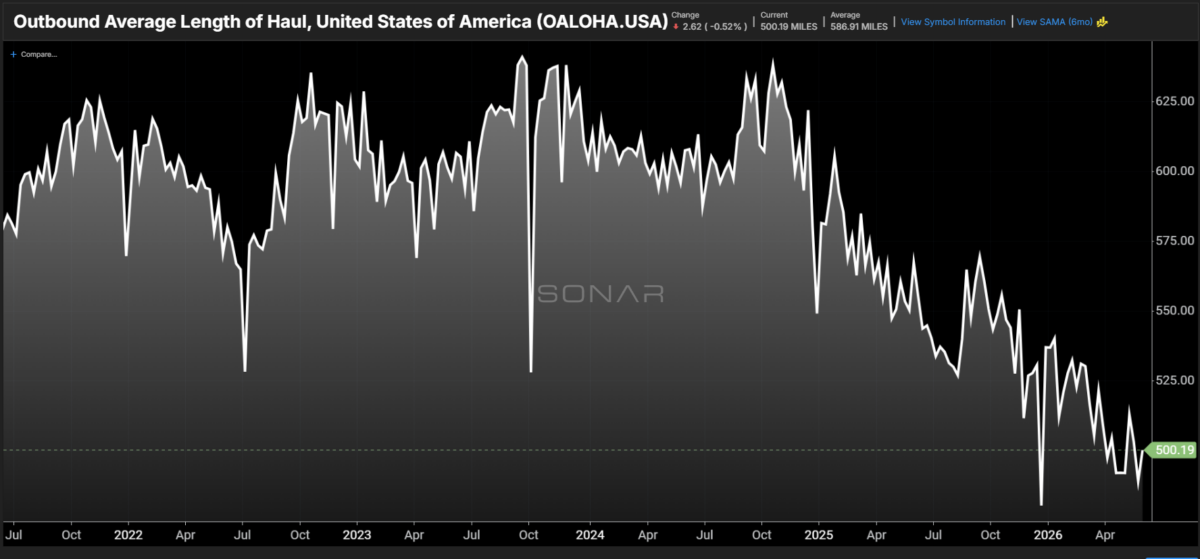

Chart of the Week: Outbound Average Length of Haul – USA SONAR: OALOHA.USA

Despite the ongoing tightening of the domestic truckload market, the trend of shrinking load lengths that began in 2024 shows little sign of reversing. Since June 2024, the average length of haul in SONAR’s tender data set has declined from approximately 607 miles to just above 500 miles — a 21% drop, with 11% of that occurring over the past year alone, making it a fairly linear trend. Is this part of a sustained structural change, or something that could flip in the near future and exacerbate current market conditions?

Perhaps the most interesting characteristic of this trend is its longevity. Most freight trends emerge sharply or follow seasonal patterns. This one looks more like a shift in how shippers utilize trucks as they adapt their supply chain management strategies — which, if true, suggests a more permanent alteration of the market.

The reason this trend matters is that longer lengths of haul occupy more capacity. Longer transit times mean trucks cannot pick up other freight. A load moving from Los Angeles to Chicago covers roughly 2,000 miles and occupies three to four days of a single truck’s time. A load moving from Atlanta to Nashville covers around 250 miles and occupies roughly half a day, depending on loading and unloading times.

In that sense, a shrinking length of haul should have freed up capacity over the past two years, as trucks are cycled more frequently — even despite the strengthening in demand seen recently (up approximately 10–15% year-over-year in early June). Yet tender rejections sit at multi-year highs above 17%, while spot rates are surging across all three main trailer types.

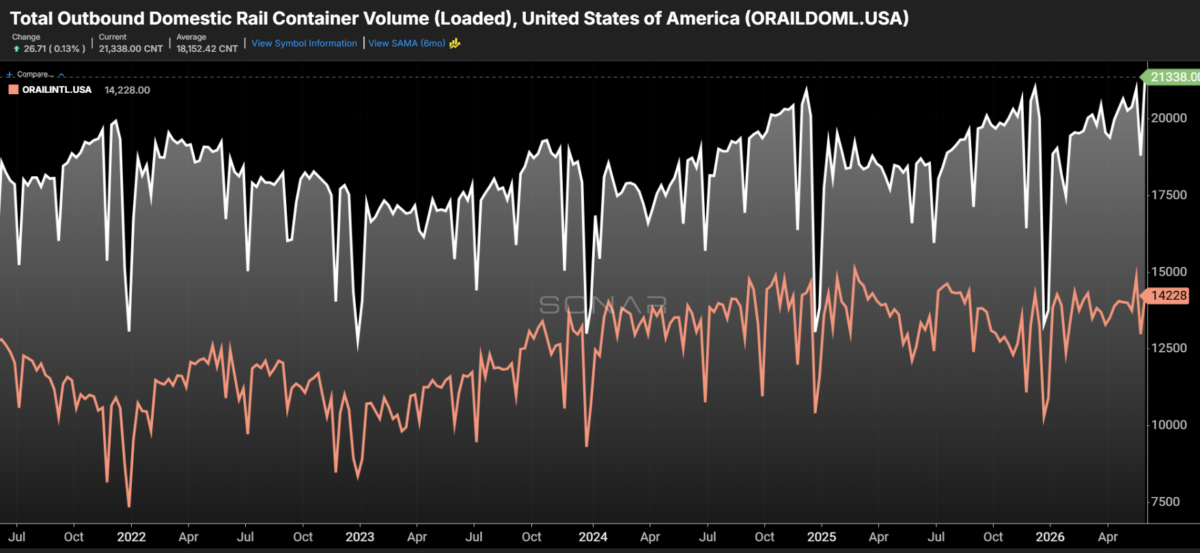

The data suggests that one driver of deteriorating load lengths is the loss of share to railroads in the form of intermodal — a topic we have covered numerous times. Intermodal holds a strong cost advantage over trucking on longer transcontinental lanes but struggles to compete on shorter distances.

Intermodal lost share to trucking during the pandemic when it couldn’t keep pace with demand. Since then, railroads and carriers have invested in infrastructure and expanded capacity to handle greater volume and demand surges. Loaded international container volumes (ORAILINTL) were up approximately 11% year-over-year last week according to SONAR’s intermodal volume data, while domestic container volumes (ORAILDOML) were up 14%.

International container volumes are a direct derivative of imports, as containers are loaded from ships and port yards directly onto trains. Domestic containers typically originate in the U.S. and are transloaded at warehouses.

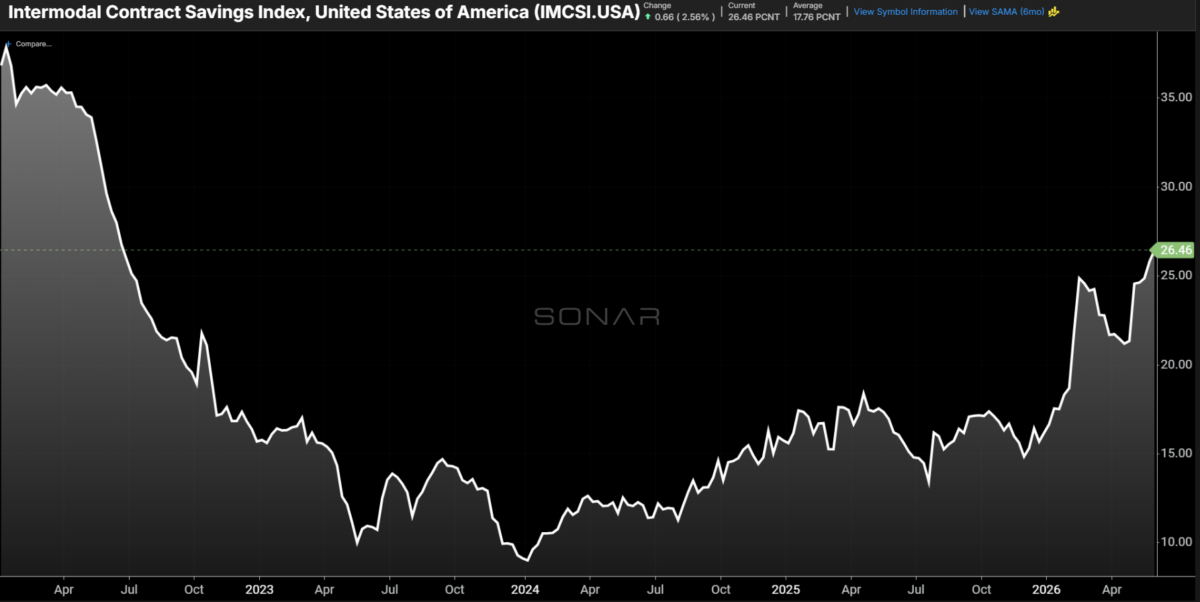

Intermodal has a cost advantage, but service favors trucking due to its ability to move directly in and out of shipper facilities with fewer touchpoints. Intermodal contract savings averaged between 10% and 20% in 2024 and 2025, but that gap has widened rapidly this year as truckload rates have climbed.

Intermodal pricing is closely tied to truckload, as railroads and carriers won’t leave money on the table. Rates are expected to rise for intermodal this year, but not enough to push loads back to trucking.

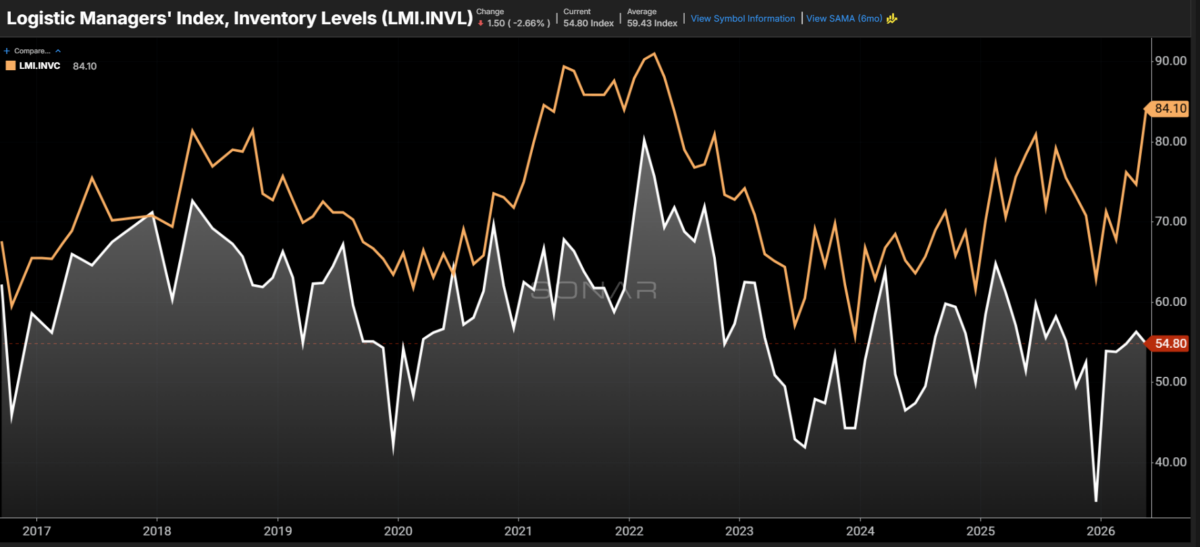

The deciding factor for whether a load moves by intermodal or truck is service. Shippers have had ample time to move freight domestically in recent years, as internationally sourced freight has been disrupted by growing global tensions. Houthi attacks in the Red Sea have altered shipping lanes for multiple years, disrupting service patterns. Unpredictable U.S. trade policy has also led many companies to import goods well ahead of expected demand. This just-in-case inventory strategy favors rail, since the extended lead time makes slower transit acceptable.

That dynamic has shifted in recent months, according to the Logistics Managers’ Index, which surveys hundreds of supply chain managers across a broad range of businesses. Inventory levels are now being managed just above replenishment as inventory carrying costs have surged.

Interestingly, this shift has not pushed load lengths higher. Imports have remained low relative to the previous two years, and most of the demand fueling the truckload market has come from moves under 250 miles, pushing carriers toward a more regionalized approach. The recent trend of shrinking load lengths is therefore less about modal shift alone and more about a disproportionate growth in short-distance moves.

Most of the retail freight that dominates the fourth quarter arrives via ship in August and September. Will trucking see a surge in long-haul demand that further deepens the current capacity crunch later in the year — and how will transportation managers respond?

A last-minute import flood could strain transportation networks later in 2025, but it is unlikely to persist, as supply chains have been permanently altered to some degree. It also makes the prospect of a transcontinental railroad merger that much more intriguing.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

The post Truckload’s shrinking miles appeared first on FreightWaves.

Continue reading...